Navigating Payment Gateway Options for MSPs: How to Make the Right Choice

The payment gateway market in the United States is valued at 38.3 billion USD by Statista. Considering its predicted compound annual growth rate (CAGR) of 22.2% between 2023 and 2030, two things are clear — the demand for payment gateways is growing, and the market is poised to meet that demand.

Choosing the right payment gateway for your MSP is important due to its financial implications. This blog post will tell you exactly that.

Considering the critical role payment gateways play in managing secure and efficient credit and debit card transactions for MSPs, this isn’t a decision to take lightly. Your business must balance aligning your operational needs with client preferences.

However, your choice becomes even more daunting with hundreds of payment gateways.

Here is your comprehensive guide to navigating the complicated payment gateway landscape and choosing the option that best meets your MSP’s needs.

{{toc}}

What is a Payment Gateway?

A payment gateway is a vital technology for an MSP. It facilitates online transactions and transfers important information between customers, merchants, and banks. Consider it the digital equivalent of a point-of-sale terminal in a brick-and-mortar business.

With the increasingly widespread adoption of mobile banking and eCommerce, Statista projects the total digital payment market transaction value will reach US $11.55 trillion in 2024.

The most straightforward way to complete these transactions is with a payment gateway.

Otherwise, merchants must rely on options that tend to be far less efficient:

- Cash on Delivery (COD)

- Bank transfers

- Checks

- Mobile wallets

Some of these options seem more secure than a payment gateway, which appeals to some. However, they lack the speed and reliability of a carefully vetted payment gateway.

For instance, both parties must be present for COD transactions, bank transfers can take days to complete, and checks can bounce.

In contrast, a payment gateway streamlines transactions by providing direct communication between all parties involved in an online transaction — from customers and merchants to banks.

To make the most of this technology, however, you must be sure your choice is customized for your MSP's unique requirements while supporting your clients' preferred payment methods.

{{ebook-cta}}

10 Key Factors to Consider When Choosing a Payment Gateway

Along with the hundreds of providers you must choose from, each payment gateway has several crucial factors to consider. Without considering all these, you risk selecting a payment gateway that doesn’t meet your needs or other mission-critical requirements.

Here, we will outline nine of the most important factors to consider when choosing between payment gateways.

Considering these factors and how they relate to your business needs helps you choose a suitable solution.

1. Security Compliance

Payment security, including fraud detection and encryption, is paramount. Companies that process, store, or transmit credit card data must comply with the requirements of the Payment Card Industry Data Security Standard (PCI DSS).

2. Risks of PCI Non-Compliance

If you choose a payment gateway that is PCI non-compliant, it opens businesses up to many unnecessary risks:

- Not complying with the PCI DSS standard can result in extensive financial penalties. The PCI SSC has the authority to impose fines of up to $500,000 per violation.

- Payment brands (Visa or MasterCard) can enforce restrictions, including not processing card payments made by non-compliant merchants.

- Data breaches are an urgent concern for payment gateways. They significantly harm a business’s reputation, resulting in extensive legal costs and other monetary penalties. PCI compliance does not completely ensure data security, but it is an important part of a comprehensive data security plan.

MSPs that store, process, or transmit cardholder data (CHD) and sensitive authentication data (SAD) must also be compliant or risk serious penalties.

If your MSP doesn’t provide proof of PCI compliance, acquiring banks could impose a penalty, billed monthly. Acquiring banks base this penalty on several factors, including the specific violation.

Again, this fee could cost a business up to $500,000 per violation, depending on the time it has been non-compliant and the severity of the non-compliance.

Your chosen payment gateway must be PCI-compliant to avoid the serious risks of non-compliance.

2. Integration Capabilities

Confirm your existing systems are compatible with a particular payment gateway.

Adopting a payment gateway for your MSP business with the appropriate integration capabilities can be seamless and successful. For instance, you would ideally want a gateway that integrates with your PSA and/or accounting tools (QuickBooks or Xero).

It is best practice to confirm whether a payment gateway offers compatible integrations for your systems before making a final decision.

3. Transaction Fees

During your research, inquire about a payment gateway’s pricing model. Some charge a flat fee per transaction, others charge based on a percentage of the transaction value, and some use both.

Neither one is outright better than the others. Depending on the size of your transactions, one is more cost-effective for your MSP.

Consider these examples broken down by fee per transaction and total monthly cost to demonstrate how different structures for transaction fees will be better for certain MSPs.

Note how different fee structures affect how much a business spends on monthly transaction fees.

Additional Fees

In addition to considering how these fees will impact your bottom line, find out about any other payment gateway fees to expect.

This includes:

- Setup fees: A one-time cost when you first sign up to cover configuration and integration processes. Payment gateways like Square and Stripe do not charge setup fees.

- Transaction fees: These can be flat fees, percentage-based amounts, or a combination of both, such as 2.9% + 30¢ per transaction.

- Monthly fees: You might be charged monthly fees for using a particular service, often no more than $25 or $30 per month.

- Chargeback fees: These fees cover the administrative costs of managing a dispute. Some platforms, including Square, cover chargeback fees for disputes. For those that do charge, these fees range from $15 to $100 per disputed transaction. Stripe, on the other hand, charges $15 per chargeback.

- Refund fees cover the cost of returning funds to a customer. They are often based on a percentage of the refunded amount.

- PCI compliance fees: A payment gateway might charge its customers to offset the cost of ensuring PCI compliance. This typically ranges from $75 to $120 per year. Others waive this cost by rolling it into other fees.

- Termination fees: These are charged if you cancel your account before the end of a contract term. Most big payment gateways, including Authorize.Net and Square, do not charge these fees.

- Miscellaneous fees: You might be charged other fees, including a foreign handling fee to accept foreign credit cards for international transactions. In this case, you might expect to pay a 1% fee per transaction for miscellaneous costs.

Note how the fee structures vary depending on the type of transaction a gateway processes.

Gateways charge higher fees for processing additional payment methods and less for ACH direct debit.

Stripe, for example, charges 80¢ per transaction for additional payment methods and 0.8% (with a $5.00 cap) per transaction for ACH payments.

Account for these fees for a particular platform and compare them to other providers to determine the most cost-efficient yet effective option.

4. User Experience and Customer Support

Look into a payment gateway’s reviews to understand how user-friendly it is. Your chosen payment gateway should be simple for your team and your clients — the faster you learn how it functions, the sooner you can make efficient transactions.

Trusted sites like Capterra, Trustpilot, and G2 can give you a better idea of the type of user experience you can expect with a payment gateway.

You’ll also find case studies that offer valuable insights into the strengths and weaknesses of different solutions. MSP-focused forums, such as this one on Reddit, can also prove to be a helpful source.

During your user experience research, look into a payment gateway’s customer support. Reliable customer support is necessary to solve payment issues as quickly as possible.

Payment gateway reviews and ratings provide valuable insight into clients' general experience with those platforms. This is a good way to spot potential red flags and highlight standout features that appeal to you.

5. Accepted Payment Options

You risk losing business if your chosen payment gateway doesn’t offer your clients’ preferred payment methods.

Most reputable gateways offer widely accepted payment methods, including Visa, Mastercard, American Express, and ACH payments.

Check the payment methods available for each payment gateway on your shortlist to see if they align with your customers' preferences.

6. Multi-Currency Support

If your MSP does business with clients worldwide, consider a payment gateway’s multi-currency support and fees for international transactions.

For example, PayPal charges a 1.50% fee for all international commercial transactions.

In addition to this percentage fee, a set fee varies depending on the currency received. PayPal charges an additional flat fee of 0.59 CAD when you receive Canadian currency and EUR 0.39 when you receive funds in Euro.

7. Settlement Period

Settlement periods impact your cash flow. If cash flow is a concern, use this factor when deciding. With a limited cash flow, paying for daily expenses, financial emergencies, supplies, and all operational expenses is difficult.

This can ultimately damage your reputation and your vendor, supplier, and client relationships. The consequences of this can include disruptions in service, loss of trust, and financial instability.

If a settlement timeline is too slow, you'll wait longer to receive payment for your services. Some payment gateways offer same-day settlements; others can take up to a week or more.

For example, PayPal does not charge a fee for standard withdrawals to a bank account or card unless currency exchange is involved, but this means the settlement period will be longer.

Funds will usually be deposited into a merchant’s account within one to three business days (for Visa and MasterCard) and between one and eight days for American Express.

For merchant account withdrawals to bank accounts, a settlement is usually posted to a merchant bank account 48 to 72 hours after settlement approval.

For those who want a faster settlement period, PayPal offers an instant withdrawal option. This option charges 1.50% of the amount transferred (and a minimum fee of $0.50).

8. Withdrawal Limits

Some payment gateways also have withdrawal limits for each transaction, day, week, and month.

For example, PayPal’s limit for daily withdrawals (in USD) is $25,000.

Consider a payment gateway’s average settlement time and withdrawal limits to ensure compatibility with your business operations.

9. Scalability

Your business is growing, and your payment gateway should, too. Choose a solution that can handle increasing transaction volumes to avoid growing pains.

One key factor to consider is your current monthly transaction volume and cost per transaction versus where you hope to be in the future.

If the total cost per transaction increases, you need to know if the payment gateway you choose has a transaction limit high enough to meet it.

Similarly, when this metric increases, you want to determine what you can expect to pay for a higher transaction volume.

Or, you need to know if the payment gateway could block your settlements altogether if you exceed your limits.

10. Transaction Limits

In addition to PayPal’s withdrawal limits listed above, it also has transaction limits. This applies to the maximum amount you can send or receive in a certain period.

Users report having their accounts limited by PayPal (so they temporarily cannot send, receive, or transfer money) if they exceed their average monthly volume.

PayPal’s transaction limits for business accounts are as follows:

- Unverified business accounts: $10,000 per transaction.

- Verified business accounts: $60,000 USD per transaction.

PayPal might also enforce limitations for suspicious activity, non-compliance, excessive claims and chargebacks, and a sudden jump in sales volume.

Also consider other scalability factors, including global expansion, performance and downtime, and the integrations you might need as your business grows.

Exploring Popular Payment Gateways for MSPs

Having covered the primary factors to consider when choosing a payment gateway, we will now move on to some of the most popular ones for MSPs.

We will present each gateway with a brief overview of its noteworthy features, prices, pros, and potential cons. You will also learn why specific payment gateways suit certain MSPs better.

1. Stripe

Stripe is a cloud-based payment processing platform that provides businesses with comprehensive tools and functionality for accepting payments online.

Customers can pay with credit cards, debit cards, ACH transfers, and alternative payment methods like Apple Pay or Google Pay.

Stripe’s pricing is based on a flat rate of 2.9% + $0.30 per transaction.

Noteworthy Features:

- Payment acceptance: Major credit and debit cards, ACH payments, and alternative payment methods.

- Fraud detection: Uses intensive fraud detection algorithms to protect against fraudulent transactions and associated charges.

- Subscription billing: Allows for easy subscription management and recurring billing.

- Developer tools: Offers a robust set of APIs and integration options for customization

Pros of Using Stripe:

- User-friendly

- Exceptional fraud detection

- Customizable developer tools

- Supports 135+ currencies

Cons of Using Stripe:

- Flat-rate pricing can add up for high-volume businesses

- Currently available in 46 out of 195 countries, which could limit global transactions

- Stripe has been known to change its rules occasionally, and you might be unsure if it will continue supporting MSPs in the future.

Who is Stripe Best For:

Smaller MSPs with a lower volume of transactions and businesses seeking advanced fraud detection capabilities.

Stripe Alternative:

- Learn more: Stripe vs. FlexPoint

2. PayPal

PayPal is one of the world's most widely recognized online payment systems. Its global recognition and broad user base make it an attractive option for MSPs. PayPal accepts major credit and debit cards and Venmo transactions.

PayPal pricing is a flat rate of 2.9% + a fixed fee per transaction that varies depending on the currency received.

Noteworthy Features:

- Payment acceptance: Major credit and debit cards and Venmo transactions.

- Subscription billing: Allows for easy subscription management and recurring billing.

- International payments: Support 25 currencies from 200 countries and allow cross-border transactions.

Pros of Using PayPal:

- Trusted and widely recognized brand

- Easy-to-use interface

- Integrations with several eCommerce platforms and business tools

- Accepts most payment methods

- Does not require a contract

- No setup fees

Cons of Using PayPal:

- Higher fees for international transactions compared to other gateways

- Potential for chargebacks

- Settlements can take two to three days

Who is PayPal Best For:

Smaller businesses are looking for a straightforward way to process transactions with no setup fees or extensive onboarding required.

PayPal Alternative:

- Learn more: Stripe vs. PayPal

3. Square

Square is another key player, having processed payments of almost $210 billion in 2023 alone.

What began as card reading technology in 2009 has now grown into a comprehensive suite of software and hardware for businesses, including managed service providers.

As for its fee structure, Square charges 2.9% + 30¢ per online transaction, 3.5% + 15¢ per manually entered transactions, and 3.3% + 30¢ per transaction for invoice payments.

Notable Features:

- Payment acceptance: Accepts all major credit and debit cards, Apple Pay, Google Pay, and gift cards.

- Customer data tracking: Collects contact information, purchase history, and other customer data.

Pros of Using Square:

- User-friendly

- No monthly or setup fees

- Offers a full suite of business tools in one platform

- Provides comprehensive sales analytics

Cons of Using Square:

- Higher fees for manually-entered transactions

- Less scalable than other options

- It may not be suitable for high-volume businesses due to transaction limits

Who is Square Best For:

Some smaller MSPs or businesses want an all-in-one solution to manage payments, inventory, and customer data. As Square’s transaction fees can add up quickly, it may also be best suited for lower volume, less complex businesses.

4. Authorize.Net

More than 445,000 merchants use Authorize.Net as their payment gateway. For its basic payment gateway plan, users pay a $25 monthly fee, transaction processing fees of 10¢, and a daily batch fee of 10¢.

It also offers plans, including a payment gateway and a merchant if you require one.

In this case, users pay a monthly fee of $25 and 2.9% + 30¢ per transaction. For users who process more than $500,000 per year, it offers customized pricing, including Interchange Plus.

Noteworthy Features:

- Payment acceptance: Most credit cards, debit payments, and electronic checks.

- Developer tools: Numerous APIs and integration options for customization.

- Fraud detection: Enhanced fraud detection algorithms protect against fraudulent transactions.

Pros of Authorize.Net:

- Fraud detection reduces the likelihood of chargebacks

- Fast settlement time—within 24 hours of the merchant capturing a transaction

- Award-winning customer support

- Offers merchant account services for a one-stop-shop solution

Cons of Authorize.Net:

- Monthly gateway fee of $25

- Extra fees for additional features like recurring billing and fraud detection

- Some users note the website lacks user-friendliness

- Setup fee of $49

Who is Authorize.Net Best For:

Smaller businesses that want a payment gateway as well as a merchant account.

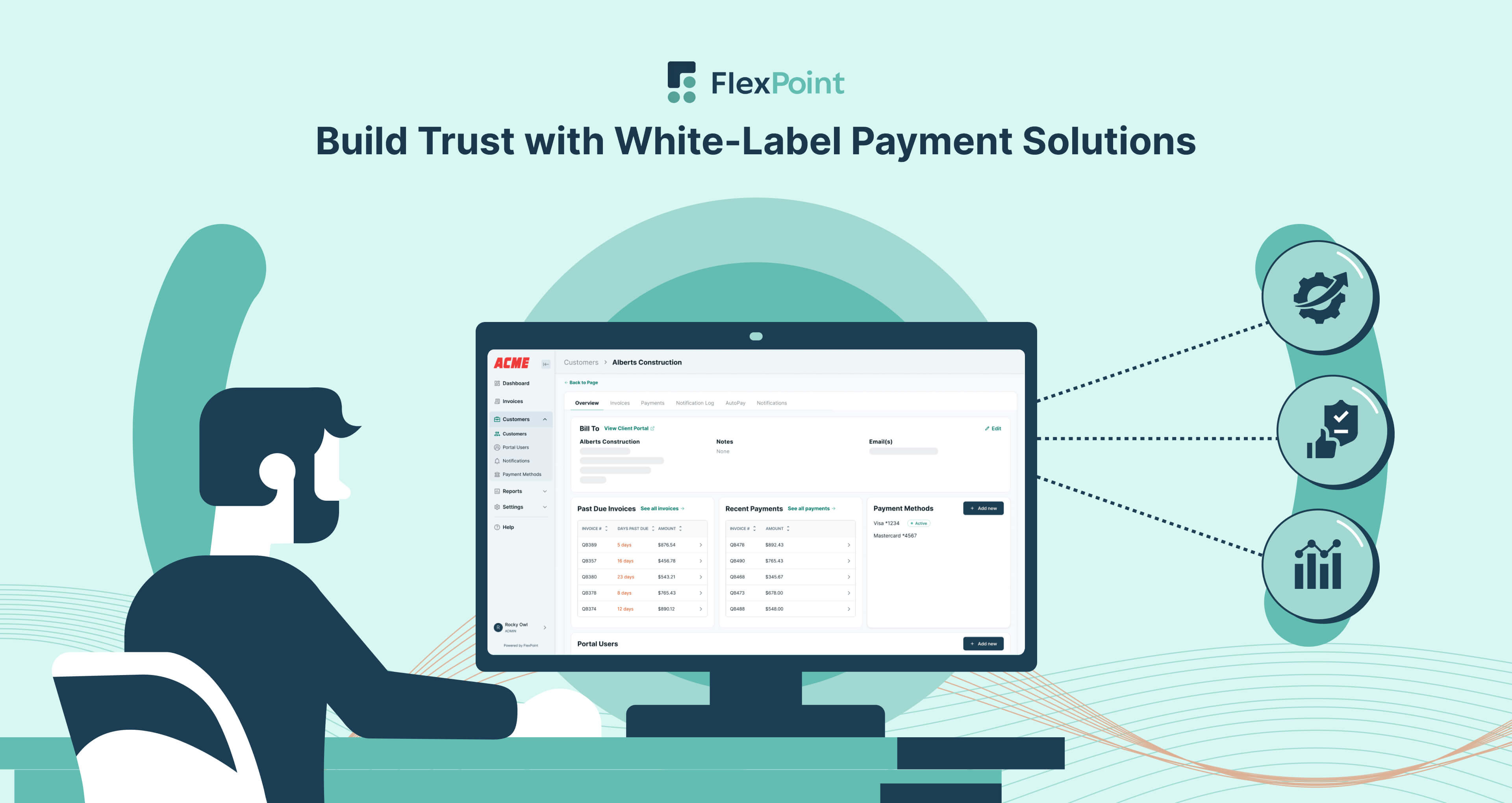

5. FlexPoint

While it may not be a payment gateway, FlexPoint is the MSP payment automation software you want to use with your chosen payment gateway.

With FlexPoint, you can automate payment processing and streamline your invoicing process. As a highly scalable option for MSP payment automation, you can trust FlexPoint to grow with your business.

Noteworthy Features:

- Recurring invoicing: Accommodate complex recurring billing structures or consistent billing cycles.

- Real-time updates: Get accurate information about payment receipts, invoice status, and overdue payments.

- Customization: Flexible invoicing workflow and reports to match your unique processes.

- Intuitive dashboards: Keep track of cash flow and working capital.

- User-friendly branded client portal: Make it easy for your MSP clients to view their invoices and make payments.

- Automation: FlexPoint can automate the entire reconciliation process from invoicing to deposits.

- Integrations: Accounting (QuickBooks Desktop, QuickBooks Online, Xero) and PSA integrations (ConnectWise, SuperOps) to meet all of your business needs. If a certain integration is unavailable, use our powerful API for custom integrations.

Pros of Using FlexPoint:

- Custom AutoPay rules

- Industry-specific software for MSPs

- Same-day payment processing approval

- Robust security and fraud-detection methods

- Multiple payment options

Cons of Using FlexPoint:

- Currently, there are limited integrations, but FlexPoint is rapidly expanding to include more platforms and tools.

Who FlexPoint is Best For:

Any MSP that wants to streamline and automate its payment processing and invoicing.

Conclusion: How to Choose the Right Payment Gateway

This blog post covered vital information about choosing the right payment gateway for your MSP.

Having covered topics like security compliance, integrations, and fees, you can make a more informed decision. An overview of popular options (Stripe, PayPal, Square, Authorize.Net, and FlexPoint) also highlighted the pros and cons to help you decide on a payment gateway.

But what if there was a solution that could go beyond just what a payment gateway offers?

This is where FlexPoint comes in.

FlexPoint addresses all the critical aspects mentioned and offers comprehensive features to streamline your MSP financial operations. With FlexPoint, you can automate invoicing, manage transactions efficiently, and scale your business within a single MSP payment system.

Enhance your MSP’s financial operations with FlexPoint. Learn more about how FlexPoint can help your business optimize payment processes.

Visit our website or contact us for a personalized consultation.

Additional FAQs: Choosing a Payment Gateway for MSPs

{{faq-section}}

.avif)