How MSPs Can Save on Credit Card Processing Fees?

Payment processors charge a fee for handling digital transactions, which accumulates quickly as a variable cost for businesses. Credit card processing fees range from 1.15% to 4% per transaction, depending on the type of transaction (card-present vs card-not-present), credit card type, industry, etc. This fee impacts the bottom line and financial health of Managed Service Providers (MSPs).

MSPs deal with high monthly transaction volumes and recurring billing models, so credit card processing fees become a substantial expense. According to the Nilson Report, in 2022, U.S. merchants paid $160.70 billion trillion in processing fees to accept card payments.

Reducing credit card processing fees helps MSPs maintain competitive pricing while improving profitability. This article will help you understand the impact of credit card processing fees on MSPs' businesses and discuss strategies they can use to mitigate these costs.

{{toc}}

The High Cost of Credit Card Processing for MSPs

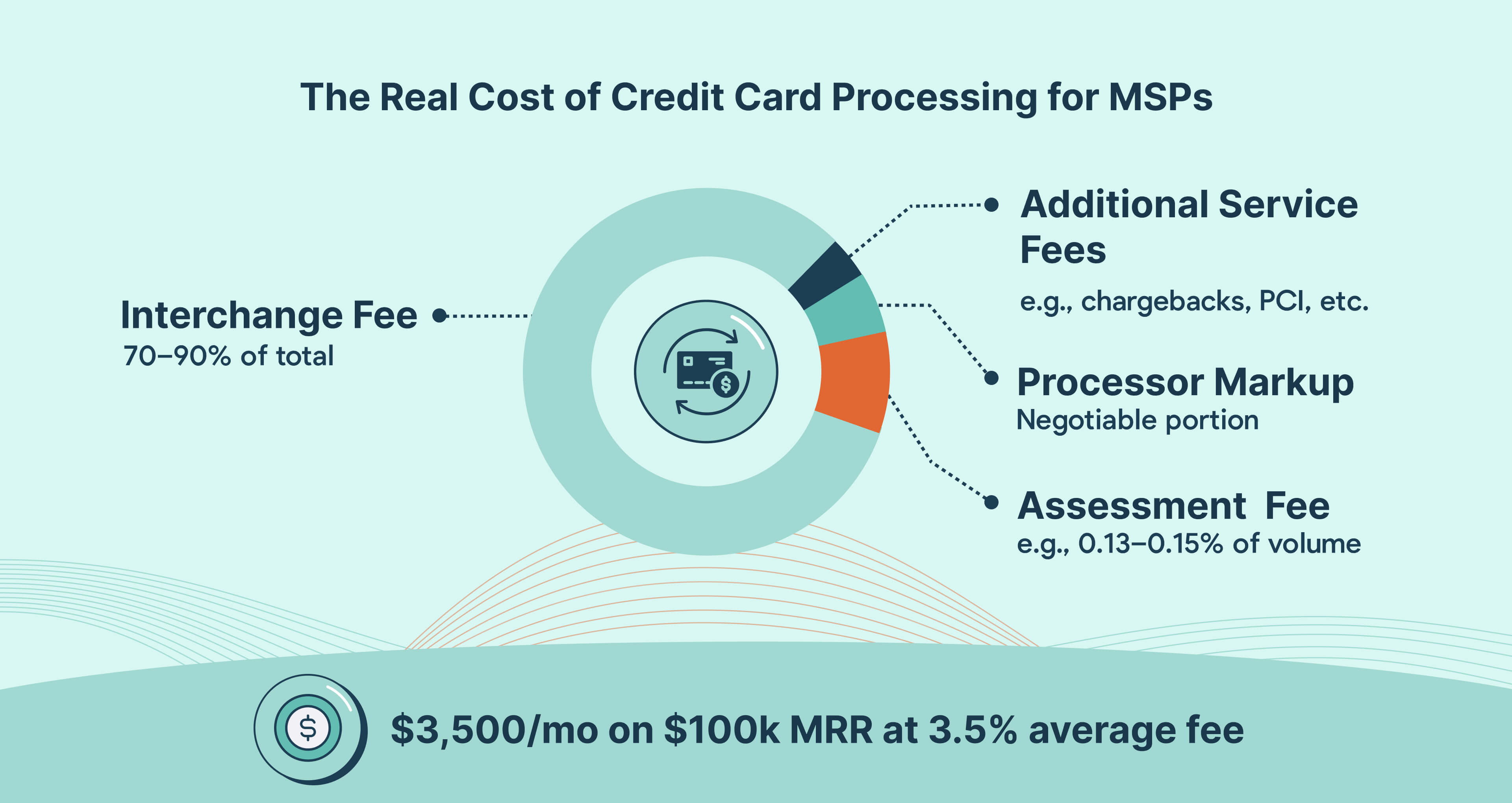

Suppose you are an MSP with a monthly recurring revenue (MRR) of $100,000.

Assuming an average transaction fee of 2%, the credit card processing fees can cost your company around $2,000 monthly.

You must review their merchant statement to understand how much they pay in processing fees. It will show a breakdown of all your transactions and associated costs. Identify areas where you incur higher fees, such as non-qualified or downgraded transactions. It will help you negotiate with your payment processor for better rates.

The key components of credit card processing fees include:

- Interchange Fees are decided by card networks such as Visa, MasterCard, and American Express and are paid to the bank issuing the customer's card. They make up 70% to 90% of the credit card processing costs. So, even reducing them a bit can result in significant savings. These fees depend on the card type, the business industry, and the transaction type. MSPs must categorize transactions correctly to prevent unnecessary interchange fees, as the costs vary depending on the risk levels. Transactions classified as higher-risk categories attract higher fees.

- Assessment Fees are charged by the card networks to operate the payments. They consist of fixed fees and a percentage of the transaction value. These are generally lower than interchange fees, but some networks may charge a higher percentage as your transaction volume grows. However, they accumulate over numerous transactions, adding to the overall cost burden on MSPs. These fees are a fixed percentage of the total transaction volume and are non-negotiable. Assessment fees for popular card networks are as follows:

- Visa: $0.0195 per transaction + 0.14% of all credit card volume.

- Mastercard: $0.0195 per transaction + 0.1275% of total card volume for transactions under $1,000 or 0.1475% of total card volume for transactions exceeding $1,000.

- Discover: $0.0195 per transaction + 0.13% of all card volume.

- American Express: 0.15% of total card volume.

- Processor Markup is a fee paid to the credit card processor for things such as Chase Merchant Services, Stripe, Moneris, Global Payments, etc. Unlike interchange fees, you can negotiate the processor markup, which means there is an opportunity for cost savings. These markups vary from one processor to another, which allows MSPs to negotiate better rates.

- Additional Service Fees are processor charges for additional services like chargebacks, retrieval requests, PCI compliance fees, and early termination. These fees add up over time, increasing total processing costs. MSPs should carefully review these additional services to determine if they are essential and consider negotiating them.

{{ebook-cta}}

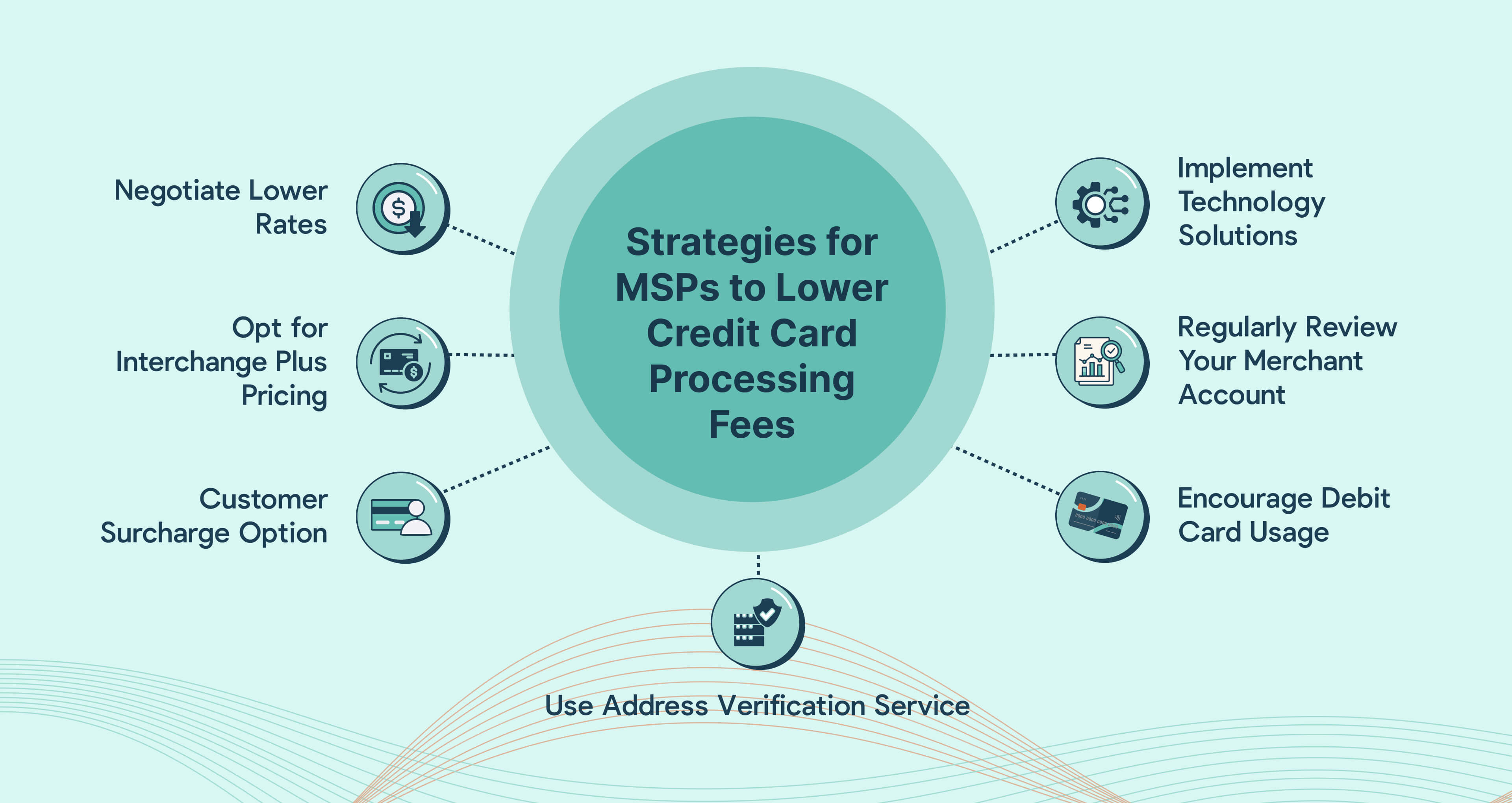

7 Strategies to Reduce Credit Card Processing Fees for MSPs

Lower fees can give MSPs more financial flexibility, enabling them to increase their profits. The savings can be invested in growth, expansion, or maintaining a competitive position. You can begin by auditing your previous statements to understand your baseline costs, including discount rates, per-transaction fees, authorization fees, and monthly fees.

Here are some strategies MSPs can use to reduce credit card processing fees:

1. Negotiate Lower Rates

A clear understanding of the merchant statement helps identify high-cost transactions.

Interchange fees account for approximately 2% of credit card processing costs in the US. MSPs must negotiate with the payment processor to reduce these rates based on transaction volumes and industry.

However, monitoring the credit card merchant statements is essential to ensure adequate negotiated lower rates. Different payment processors offer varied interchange fees, so you should switch to a more feasible option.

Let’s say you’re an MSP that processes $100,000 transactions monthly. You pay an average of 2.9% in fees for every credit card transaction—or about $2900 monthly in processing fees.

If you can negotiate a fee reduction of 0.2% (down to 2.7%), the savings will amount to $200 per month — a difference that adds up over time.

In a few cases, vendors will often provide a cost-savings comparison using your current merchant services statements. They will review your current transaction volume and pricing structure and then provide you with a potential ROI report for switching providers.

2. Opt for Interchange Plus Pricing

Interchange Plus (IC+) pricing is a transparent model that separates interchange fees from processor markup. It works with business-to-business (B2B) transactions and allows businesses to see the actual cost of processing each transaction. It becomes easier to identify high-cost transactions and compare processors.

In the case of interchange plus pricing, businesses pay the actual interchange fees set by card networks plus the processor's fixed markup fee.

For major payment networks (Visa, Mastercard, American Express, Discover), interchange fees are often between 1.0% and 3.15%.

Importantly, there are exceptions, including Mastercard’s offer of 0.00% + $0.75 for American customers who pay utility bills with credit, and this varies from industry to industry (or MCC - Merchant Category Code). Based on our research, such exceptions are not available for IT solutions providers or MSPs.

A fixed markup fee in interchange plus pricing is beneficial because it offers clarity and predictability. You will know what to expect regarding additional costs over the interchange fees.

Simply put, interchange plus pricing is much more straightforward than other models.

MSPs can use lower interchange fees through level II and III data processing. These data types provide richer transaction information such as:

- Level II Data: Tax indicator and amount, customer code for transaction tracing, and purchase order number

- Level III Data: Discount amount, shipping amount, product code, description, quantity, and unit price

Card networks offer lower interchange rates in exchange for data. With level III data processing, MSPs can save up to 1% on the transaction’s value.

3. Customer Surcharge Option

MSPs can pass on the burden of credit card processing fees by adding a surcharge to each transaction. Set up a surcharge program that automatically adds the complete or partial fee to credit card transactions.

Note: Each US state has its own regulations for allowing credit card surcharges.

Some states permit surcharges under specific conditions.

Conversely, others ban any unexpected costs to protect customers.

MSPs must ensure compliance when implementing surcharge programs to avoid risking penalties or damaging customer trust.

The rules and laws vary from state to state.

For instance, surcharging is completely banned in Connecticut, Maine, Massachusetts, and Puerto Rico.

On the other hand, Colorado allows credit card surcharges of up to a flat 2% or allows you to charge the total actual cost of processing.

It’s important to understand the laws of the respective state on customer surcharging.

Check out our comprehensive guide on Customer Surcharging: A State-by-state Guide.

If you choose to surcharge credit card payments, then It's important to notify the credit card networks about introducing the surcharge program.

Ensure that your digital payment systems are updated to automatically include the surcharge when a credit card payment is made.

Inform your clients about the surcharge amount, helping them understand that this fee is for the convenience of using credit card payments.

4. Use Address Verification Service (AVS)

AVS, or Address Verification service, verifies the customer's billing address with the card issuer in real time to authenticate transactions. It reduces credit card fraud risk and saves you from the additional burden of chargeback fees in case of disputes.

Chances of credit card fraud and chargebacks are higher if it is a card-not-present transaction. Processors charge lower rates for verified transactions, so MSPs can use it for fraud protection and reducing processing fees.

A minimal AVS fee applies to different payment scenarios. For instance, Mastercard charges $0.01 for card-not-present transactions and $0.005 for card-present transactions. Since the cost is fixed, it prevents unexpected expenses, as some banks charge extra for transactions without AVS.

5. Encourage Debit Card Usage

Debit card transaction fees are around 21 cents per transaction and a cent for fraud prevention. It is lower compared to credit card transactions. They are transparent and less susceptible to chargebacks. Debit cards also reduce the need for costly security measures through PIN verification, reducing fraud risk.

MSPs can improve customer experience by offering debit card transactions as an alternate payment method.

Generally, debit card transaction fees are lower than those for credit cards. This can result in substantial cost savings, especially for MSPs with high transaction volumes.

Debit card transactions are typically linked directly to the funds in a customer's bank account, which can lead to fewer chargebacks initiated by the customer. Chargebacks can be costly and time-consuming for businesses to handle.

In addition, clients might prefer using debit cards as a way to manage their spending more effectively, avoiding the potential for accruing business debt associated with credit cards.

6. Regularly Review Your Merchant Account

Evaluate your discount rates per transaction, authorization, and monthly fees. Compare them against the industry standards to identify areas where you might be overpaying.

Eliminating hidden fees or surcharges helps MSPs reduce processing costs and maintain a lean fee structure.

Regularly auditing your merchant account to monitor transaction fees helps ensure you are paying for only necessary services.

Here are some of the charges to watch for:

- Higher-than-expected transaction fees

- Monthly minimum fees even if your transaction volume meets the minimum threshold

- Unexpected PCI compliance fees (these fees ensure your merchant account meets PCI DSS requirements)

- Undisclosed batch processing fees

- Paper statement fees, even if you have opted to receive them electronically

Your merchant account provider might be linked to a specific bank. If so, this gives you additional leverage to get a better rate.

7. Implement Technology Solutions

Advanced technology, such as MSP Payment Platforms, can help you minimize transaction fees, reduce errors, and ensure faster processing times. These platforms automate the handling of large volumes of transactions and provide real-time data analytics. Automation can save up to 17 hours per week by eliminating errors due to manual data entry.

You can save costs by reducing manual errors, data discrepancies, and chargebacks. It allows for handling more clients without increasing the administrative workload. Additionally, it improves customer satisfaction by enhancing payment processing accuracy and boosting transaction speed.

MSPs need sophisticated payment management software to optimize the transaction process. The software must automate critical functions to enhance payment accuracy and lower processing fees. Increasing transaction accuracy helps control payment processing costs by reducing manual errors and chargebacks.

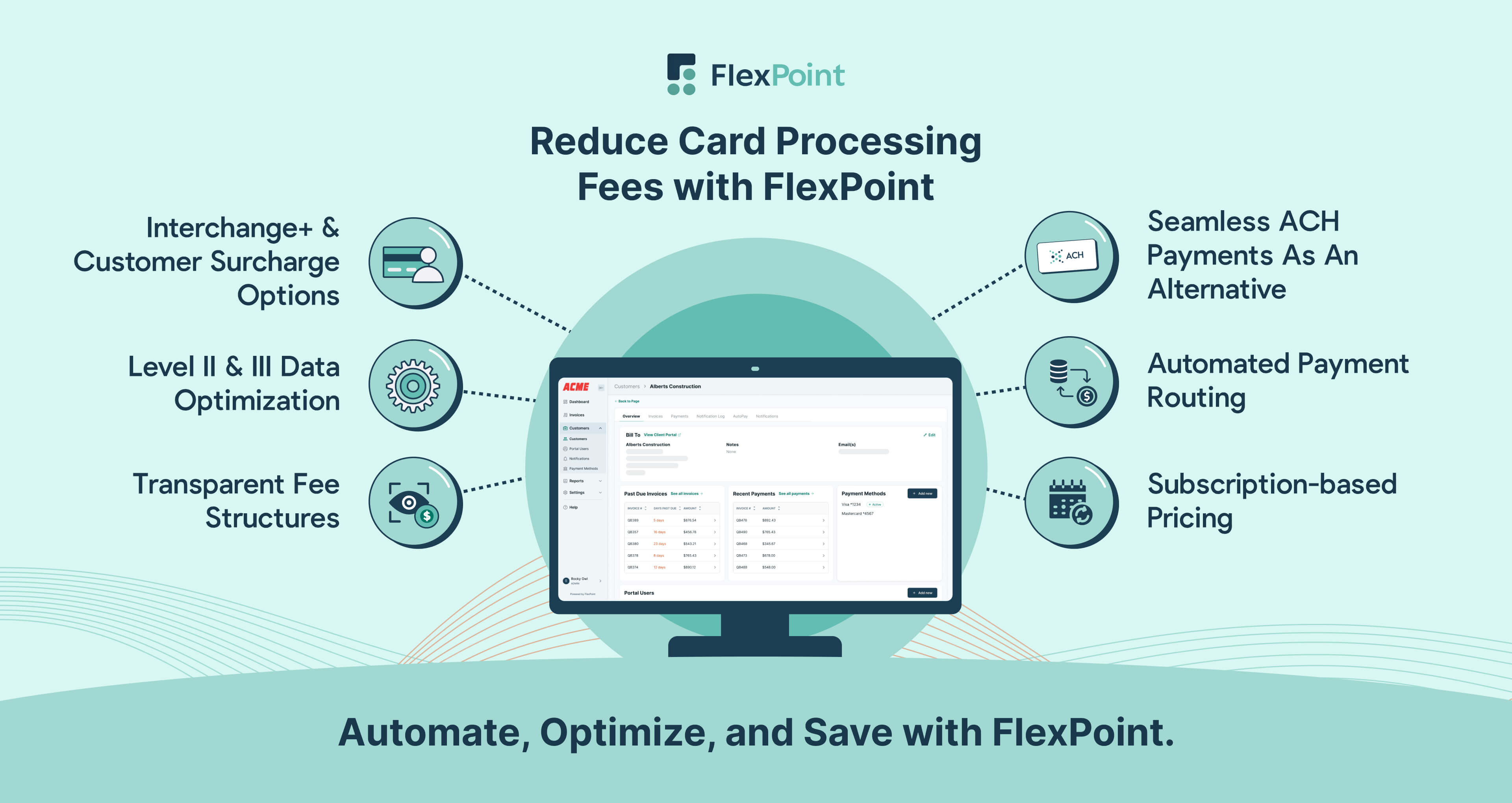

How FlexPoint Reduces Credit Card Processing Fees?

FlexPoint's MSP Payment Automation Software provides MSPs with a comprehensive platform that optimizes payment processing, reduces errors, and mitigates risks.

FlexPoint helps MSPs minimize credit card processing fees by automating large volumes of credit card transactions.

FlexPoint's payment gateway options that are useful for data management and lowering interchange rates are:

1. Interchange+ and Customer Surcharge Option:

FlexPoint's Interchange+ is an optimization strategy that helps get the best rates.

To offer more competitive interchange-plus rates, FlexPoint utilizes not only Level 1 data but also Levels II and III.

- Level I data includes real-time pricing and volume information.

- Level II includes even more information, such as merchant postal codes, customer codes, and tax amounts.

- Finally, Level III data includes line-item transaction details, product descriptions, prices, quantities, etc.

FlexPoint's Customer Surcharge Plan is designed to help MSPs completely or partially pass on the burden of processing fees to their customers. MSPs can seamlessly add a surcharge to each transaction without manual intervention. The platform automatically calculates the surcharge amount based on your business preferences and local regulations.

2. Transparent Fee Structures:

FlexPoint's fee structure helps businesses save costs. MSPs can maintain a lean payment processing system and avoid paying for unnecessary services.

FlexPoint's fee structure is designed to give MSPs the best credit card processing pricing without compromising quality.

3. ACH Payments:

FlexPoint offers lower processing fees for ACH payments than traditional credit card transactions.

ACH payments fees are typical lower than credit card payments. For instance, ACH payments through FlexPoint cost $0.25 per transaction.

Opting for an alternate payment method like ACH payments can help MSPs save costs as transaction volumes grow.

For instance, Excellent Networks, an El-Paso Texas-based MSP, saved $10,000 in annual credit card processing fees with FlexPoint’s ACH option.

Let’s use an example to examine a transparent payment option that might benefit your MSP’s transaction processing costs.

Let’s suppose you used a payment gateway with a fee structure such as this:

- ACH bank transfers: 1%

- Credit card transactions: 3.4% + 15¢

Now, let’s say you process $100,000 in monthly volume split over 40 transactions of $2,500 each, broken up like this:

- 50% ($50,000), 20 transactions processed via ACH bank transfers

- 50% ($50,000), 20 transactions processed via credit card transactions

These numbers would translate to the following processing fees:

Total Monthly Cost:

- ACH: $500

- Credit Card Processing: $1703

Total Monthly Processing Costs:

- $500 + $1703 = $2203

Annual Cost:

- $2203 x 12 = $26,436

Now, let’s use the same example with an MSP payment automation tool like FlexPoint, which offers ACH payments at only $0.25 cents per transaction; your clients might opt for this method for all 50 transactions.

Then, your fees could look like this:

ACH ($0.25 per transaction):

- ACH Fees ⇒ 40 transactions x $0.25 = $10

- Software Subscription Fees ⇒ Around $250

Total Monthly Processing Costs:

- $260

Annual Processing Costs:

- $260 x 12 = $3120

This translates to $23,316 in annual savings on processing fees with FlexPoint compared to another credit card payment gateway.

Note: The software subscription fees vary based on your monthly volumes and your chosen feature set. Contact us for a personalized quote for your specific MSP.

Conclusion: Reducing Credit Card Fees & Enhancing MSP Profitability with FlexPoint

Regular monitoring and proactive management of credit card processing fees are necessary for MSPs to maintain profitability. The savings are added to the company’s profit margin and play a critical role in its sustainability.

By reducing chargebacks, allowing ACH payments, and negotiating fees with payment gateways and processors, you know more about the available cost-saving tools.

With the right MSP payment platform, you can quickly improve your profitability rather than being slowed down by inefficient payment processes and hefty credit card processing fees.

FlexPoint gives you everything you need in an MSP payment platform, along with several features you didn't realize you wanted.

For MSPs like Net-Tech, which streamlined its payment process with FlexPoint, the benefits translated to savings on processing fees and significant time savings.

As a result, Net-Tech saved thousands of dollars in processing fees. Net-Tech also received payments 20 days faster than before, and invoicing became 80% faster.

FlexPoint’s suite of tools helps you balance service excellence and cost-efficiency. The advanced payment processing technology helps with surcharge automation while maintaining transparent fee structures.

FlexPoint's customer-centric approach allows for fee reduction with Interchange+ and alternative methods like ACH payments.

The platform provides sophisticated analytics for actionable insights such as cash flow predictions, client preference trends, and accounts receivable (A/R) reports, paving the way to more intelligent financial decisions.

Start reducing MSP credit card processing fees with FlexPoint today.

Learn more about reducing credit card processing fees with FlexPoint.

Visit our website or contact us to see how our solutions can improve your financial operations!

Additional FAQs: Reducing Credit Card Fees for MSPs

{{faq-section}}

.avif)