As of February 2025, credit card surcharging is permitted in Utah, thus providing managed service providers (MSPs) with a way to recover payment processing fees.

Instead of absorbing these costs into service pricing, surcharging enables MSPs to pass the expense onto clients who choose to pay with credit cards. This approach helps businesses preserve their profit margins and maintain predictable operating costs while offering clients flexible payment options.

To implement surcharging properly, Utah MSPs must comply with federal regulations, state consumer protection laws, and card network guidelines set by Visa, Mastercard, American Express, and Discover.

Proper disclosure, transparent invoicing, and accurate fee calculations are essential to ensure compliance and maintain client trust.

This guide details Utah’s surcharging regulations, provides strategies for introducing surcharges to clients, and explains how FlexPoint simplifies the process of managing these fees.

Disclaimer: This content is for informational purposes only and should not be considered legal advice. Utah MSPs should conduct due diligence and consult a qualified legal professional to ensure compliance with all applicable laws before implementing surcharging practices.

{{toc}}

What is Credit Card Surcharging for MSPs in Utah?

Credit card surcharging allows Utah MSPs a way to manage rising credit card processing costs. It enables them to recover fees while keeping pricing structures competitive and sustainable.

Credit card processing fees typically range from 2% to 4% per transaction and include various costs, such as interchange fees, network fees, and processor markups.

These expenses can accumulate rapidly, especially for MSPs handling recurring payments or large transaction volumes.

Consider a Utah MSP processing $95,000 in credit card payments each month. With an average processing rate of 3.1%, this MSP pays $2,945 in monthly fees. This adds up to $35,340 annually in credit card processing costs.

Suppose the MSP applies a 3.1% surcharge.

In that case, those fees are shifted to clients, allowing the MSP to retain an additional $35,340 per year—funds that could be redirected into growing the business.

Some MSPs prefer to split the costs with clients rather than pass the full surcharge.

For example, if the same Utah MSP applies a 1.6% surcharge, clients cover $1,520 per month while the MSP absorbs the remaining $1,425.

Over a year, this approach saves the MSP $18,240, thus diminishing the overall financial burden of credit card payment acceptance.

Transparent communication with clients is necessary regardless of an MSP's surcharge strategy. Proper disclosure, itemized invoices, and clear payment policies build trust and prevent potential misunderstandings.

Understanding Credit Card Surcharging Laws in Utah

Utah permits credit card surcharging, allowing managed service providers to pass processing fees to clients who pay with a credit card.

However, the legal status of surcharging in Utah has changed over time, making it crucial for MSPs to stay informed about past and potential future regulatory shifts.

Utah briefly prohibited the practice. In 2013, Utah lawmakers passed a law banning credit card surcharges on transactions of $10,000 or less. This made Utah one of a handful of states at the time that imposed restrictions on businesses adding fees to credit card transactions.

However, the law was intentionally temporary—a sunset provision ensured it would expire unless renewed by lawmakers. By July 2014, the ban automatically expired because Utah legislators chose not to extend it.

As a result, surcharging once again became permitted in Utah, with no additional state-imposed restrictions beyond existing federal and card network regulations.

Since then, Utah has not enacted new laws regulating surcharges, leaving MSPs free to implement them as long as they follow federal guidelines and card network policies.

Although Utah does not impose additional state-specific restrictions, MSPs must follow:

Federal regulations prohibit surcharges on debit and prepaid cards under the Durbin Amendment of the Dodd-Frank Act. MSPs cannot add surcharges to these card types even if processed as a "credit" transaction.

A federal surcharge cap of 4% means that an MSP cannot charge a higher fee, even if their processing costs exceed that amount.

Card network rules, which override federal limits when lower, include:

- Visa limits surcharges to 3% for Visa transactions.

- Mastercard allows surcharges up to 4%, as long as the fee does not exceed actual processing costs.

MSPs must ensure surcharges do not exceed the lesser of their actual processing costs or the applicable network-imposed limit.

Again, while Utah does not impose additional disclosure requirements, MSPs must still follow federal and industry transparency rules when applying surcharges.

Failing to follow these requirements can lead to chargebacks, client payment disputes, and potential regulatory scrutiny from consumer protection agencies.

Although Utah has no current state-level surcharge restrictions beyond general consumer protection laws, MSPs should remain vigilant about potential regulatory updates.

While no active legislative proposals seek to reintroduce a surcharge ban, Utah’s brief ban in 2013–2014 suggests that future changes are always possible.

MSPs can also monitor updates from the Utah Division of Consumer Protection, which oversees business practices and could issue guidance on surcharge-related transparency or fairness.

Utah MSPs that follow these best practices can implement surcharging effectively while maintaining compliance, reducing processing expenses, and preserving strong client relationships.

Disclaimer: This content is for informational purposes only and does not constitute legal advice. Utah MSPs should consult a qualified attorney to ensure full compliance with all federal, card network, and state consumer protection requirements.

Implementing Credit Card Surcharging for Utah MSPs

Managing credit card transaction fees presents a considerable challenge for managed service providers in Utah, particularly when handling substantial payment volumes.

Implementing surcharges helps offset these costs, but careful execution is paramount to prevent client dissatisfaction and ensure compliance with regulations.

Introducing surcharges without transparent communication leads to confusion, disputes, and potential loss of business.

Studies reveal varied consumer reactions to surcharging. For example, data from PYMNTS reports mixed feelings toward surcharging—76% of consumers say surcharges would make them reconsider using credit cards. Conversely, 40% would actively seek alternative businesses to avoid the fee.

If surcharges are not communicated effectively, clients may perceive them as an unnecessary markup rather than a way to offset payment processing costs.

To implement surcharging successfully, Utah MSPs should be transparent about their policies, clearly outlining the purpose of these fees and how they contribute to maintaining competitive service pricing.

Rather than increasing service rates across the board or absorbing transaction fees as an operational expense, shifting these costs to clients who opt for credit card payments ensures those benefiting from the convenience bear the associated costs.

The following steps provide best practices for applying surcharges while ensuring billing clarity, fairness, and compliance.

Step 1: Develop a Comprehensive Surcharge Policy

A well-structured surcharge policy promotes consistency and compliance. This policy should detail when surcharges apply, the specific percentage or fee structure, and the method of client notification.

Incorporating this policy into client agreements sets clear expectations and reduces potential misunderstandings.

MSPs may consider various surcharge models:

a) Fixed Percentage Surcharge

A consistent percentage is added to all credit card transactions.

Example: A 2.9% surcharge on a $12,000 invoice adds $348, bringing the total to $12,348.

b) Tiered Surcharge System

The surcharge percentage varies based on the invoice amount.

Example:

- 2.2% surcharge for invoices under $5,000

- 3% surcharge for invoices $5,000 and above

So, a $4,500 invoice incurs a $99 surcharge (2.2%), totaling $4,599, and a $7,800 invoice incurs a $234 surcharge (3%), totaling $8,034.

c) Flat Fee Surcharge

A fixed amount is added to each transaction, ensuring it does not exceed actual processing costs.

Example: A $35 surcharge applies to all credit card transactions.

- A $3,200 invoice totals $3,235 (with a 4% cap of $128).

- A $9,600 invoice totals $9,635 (with a 4% cap of $384).

Regardless of the chosen method, surcharges must not exceed actual processing costs.

For example, if a $1,500 transaction incurs a 2.8% processing fee ($42), a $50 surcharge would violate Visa and Mastercard rules. The fee must be adjusted to $42 to stay compliant.

Step 2: Notify Credit Card Networks and Clients

Utah MSPs are required to inform credit card networks, such as Visa and Mastercard, at least 30 days before implementing surcharges. This ensures adherence to card network policies and prevents unforeseen complications.

Effective client communication is just as vital. MSPs should clearly articulate the purpose of surcharges, stressing that they are intended to offset processing fees rather than generate profit.

A lack of transparency can lead to chargebacks, which cost businesses an average of $190 per dispute.

For example, an $8,900 invoice with a 2.8% surcharge should list the $249.20 fee separately.

If the surcharge is not disclosed clearly, a client may dispute the transaction, resulting in a chargeback. This would force the MSP to refund the amount and lead to additional processing penalties.

Step 3: Update Invoicing and Billing Systems

Invoices should always include a separate line item for surcharges to provide transparency—this cannot only be disclosed to the client on the receipt after the payment is processed.

Utah MSPs should update their invoicing and billing systems to ensure surcharges are applied accurately and consistently across all transactions.

An effective invoice should clearly display the following:

- Managed IT Services: $14,500

- Credit Card Surcharge (3%): $435

- Total Due: $14,935

This reduces the risk of disputes and keeps the payment process seamless for both MSPs and their clients.

Step 4: Monitor and Ensure Compliance

Regulations around credit card surcharging can change, just as they did in 2013-2014, and MSPs must stay updated to remain compliant.

For example, in 2023, Visa lowered its maximum surcharge from 4% to 3%. In turn, MSPs had to adjust their surcharging policies. MSPs that failed to update their surcharge rates risked fines, penalties, and even loss of payment processing privileges.

MSPs should take proactive measures to ensure their practices remain within legal and industry standards.

Regularly evaluating surcharge practices helps Utah MSPs avoid penalties, maintain transparency, and ensure a seamless payment experience for their clients.

The Role of FlexPoint in Optimizing Credit Card Surcharging for Utah MSPs

Some managed service providers in Utah rely on recurring credit card payments to maintain a steady cash flow, but processing fees from these transactions can significantly cut into profits.

As credit card usage grows, these expenses become more challenging to ignore.

Managing surcharges and processing costs manually can lead to billing inconsistencies, calculation errors, and unnecessary financial strain.

FlexPoint eliminates these challenges with automated payment solutions designed specifically for MSPs. These solutions include different payment processing plans to choose from based on an MSP’s unique situation.

Flexible Payment Processing Plans

FlexPoint provides two customized payment plans, allowing MSPs to choose whether to absorb processing costs at a lower rate or shift them to clients using surcharges.

- Interchange+ Plan

- Customer Surcharge Plan

a) Interchange+ Plan

For MSPs that prefer to absorb processing fees rather than pass them to clients, the Interchange+ plan calculates costs based on real-time interchange rates.

Because different credit cards carry different interchange fees, costs fluctuate depending on the type of card used for payment.

For instance, a Utah MSP processing $80,000 in monthly credit card payments may see lower fees on Visa debit transactions, which carry reduced interchange costs.

However, payments made with premium rewards credit cards—such as a high-tier American Express business card—will trigger higher interchange fees, increasing overall processing expenses.

Using Interchange+, Utah MSPs can optimize their fee structure by minimizing unnecessary markups, ensuring they only pay the actual processing cost rather than inflated flat-rate fees.

b) Customer Surcharge Plan

For MSPs looking to offset processing fees entirely, the Customer Surcharge Plan shifts the cost to clients.

With a fixed surcharge percentage applied to credit card transactions, Utah MSPs eliminate payment processing as an overhead expense, helping to stabilize margins and protect profitability.

Example:

A Utah-based MSP issues a $12,500 invoice. If a 3% surcharge is applied, the additional $375 brings the total to $12,875.

For MSPs that want to maintain strong client relationships while reducing financial strain, FlexPoint allows for a shared-cost model. Instead of passing the entire processing fee to clients, MSPs can absorb a portion while clients cover the rest.

Example:

A Utah MSP processing $50,000 in credit card payments applies a 1.8% surcharge to transactions while absorbing the remaining 1.2%.

This hybrid approach results in:

- Client-covered fees: $900 per month

- MSP-covered fees: $600 per month

- Annual savings for the MSP: $10,800

How FlexPoint Enhances Surcharging Compliance and Transparency

Managing credit card surcharges requires precision to stay within federal regulations, Utah laws, and card network policies.

FlexPoint automates surcharge calculations to ensure that fees remain within the 4% federal cap, simplifies invoicing, and prevents disputes caused by miscalculations or unclear billing.

To illustrate how automated surcharging works in practice, here’s an example of a Utah MSP invoice using a 3% surcharge on client transactions. This ensures that processing fees are recovered without inflating base service costs.

Utah MSP Client INVOICE

Company Name: [Your MSP]

Invoice #: 029471

Invoice Date: April 1, 2025

Due Date: June 1, 2025

Bill To:

[Client Company Name]

[Client Address]

[Client Contact Name]

[Client Email]

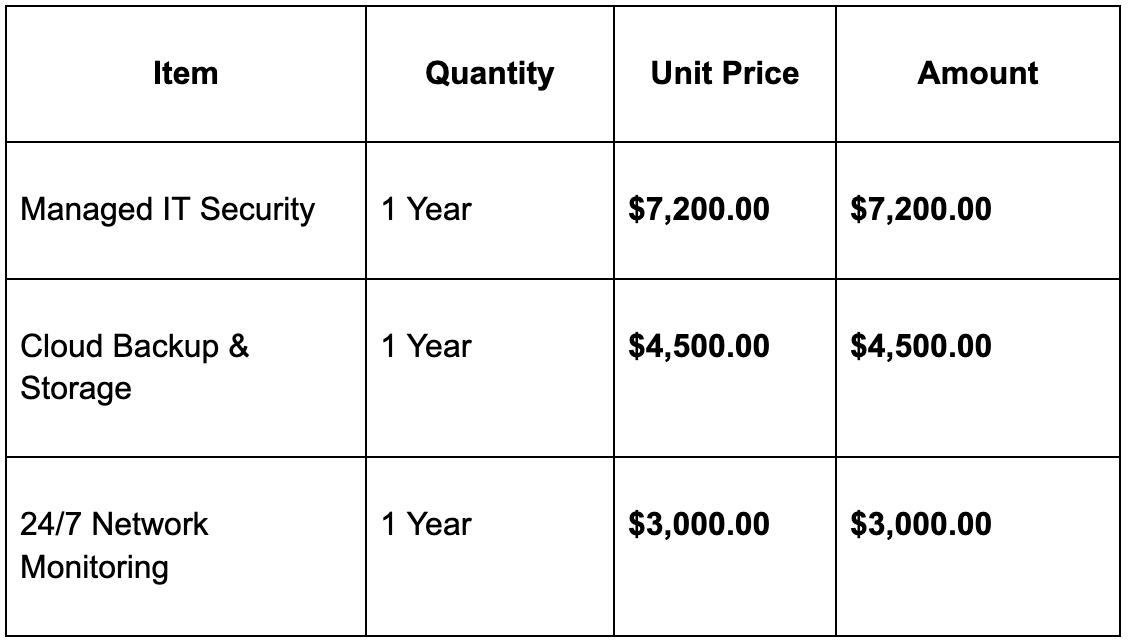

Services Provided:

- Managed IT Security

- Cloud Backup & Storage

- 24/7 Network Monitoring

Subtotal: $14,700.00

Surcharge (3% of Subtotal): $441.00

Total Due: $15,141.00

Payment Terms:

Payment is due within 60 days of the invoice date. The surcharge complies with federal regulations (4% cap), Utah’s legal framework, and card network rules.

Notes:

Thank you for choosing [Your MSP]! If you have any questions regarding this invoice, please contact us at [Your Contact Information].

FlexPoint’s Integration with MSP Tools for Seamless Billing

FlexPoint integrates with leading financial and business management tools, allowing MSPs to automate payment processes without disrupting existing workflows.

By eliminating the need for manual data entry, reducing errors, and ensuring compliance with surcharging regulations, FlexPoint helps MSPs in Utah streamline operations and focus on growing their business.

FlexPoint connects seamlessly with:

- QuickBooks Desktop

- QuickBooks Online

- Xero

- ConnectWise

- SuperOps

- HaloPSA

- Autotask

With these integrations, Utah MSPs can consolidate invoicing, billing, and reconciliation into a single automated process, eliminating manual data entry and reducing administrative overhead.

For example, FlexPoint automatically syncs surcharge details, service fees, and payment statuses when integrated with QuickBooks Online.

This ensures that financial records stay accurate without requiring manual updates, reducing the risk of errors that could lead to chargebacks or compliance issues.

Instead of manually adjusting invoices and reconciling payments, Utah MSPs benefit from real-time financial tracking that simplifies bookkeeping, enhances reporting accuracy, and supports better business decision-making.

Beyond automation, FlexPoint offers additional features that enhance financial transparency and client satisfaction:

- Branded Client Payment Portals: Clients can view invoices, update payment methods, and complete transactions through a secure, professional, and user-friendly portal.

- Real-Time Reporting: Provides up-to-the-minute financial insights, helping MSPs monitor revenue, surcharges, and outstanding balances effortlessly.

Offering Flexibility in Surcharging

Managing credit card surcharges effectively requires a balanced approach—one that allows MSPs to recover processing fees without compromising client relationships.

FlexPoint’s customizable surcharging features enable Utah MSPs to fine-tune their approach based on client needs, payment preferences, and business priorities.

For instance, an MSP may choose to waive surcharges for long-term clients with high-value contracts while applying standard fees to one-time or infrequent clients.

This flexibility helps MSPs manage costs strategically while maintaining client satisfaction and retention.

Keeping up with card network surcharge policies can be challenging, but FlexPoint’s automation ensures every surcharge is applied accurately and within compliance limits.

Utah MSPs reduce the risk of billing disputes, regulatory fines, or unintentional overcharges by removing manual calculations and automating compliance.

One of the most significant benefits of FlexPoint is its client-friendly payment experience. This level of transparency prevents misunderstandings, strengthens client trust, and reduces billing disputes.

Consider a Utah-based business that regularly pays its MSP with a Mastercard—incurring a 4% surcharge. The client realizes they can reduce this cost by switching to a Visa card, which is capped at 3%.

Using FlexPoint’s self-service portal, the client updates their preferred payment method without needing to contact the MSP. The next invoice reflects the lower 3% Visa surcharge, reducing their transaction fee while maintaining convenience.

Similarly, suppose a client’s credit card is set to expire. In that case, they can update their payment details directly in the portal, ensuring seamless billing without disruptions or manual intervention from the MSP.

By allowing clients to view, manage, and adjust payment methods in real time, FlexPoint eliminates unnecessary delays, reduces administrative workload, and strengthens client relationships.

Conclusion: Streamlining Payments with Effective Surcharging Strategies

Success with credit card surcharging depends on implementing a compliant and well-structured surcharging policy. Transparency with clients is key—unexpected fees can lead to disputes or strained relationships.

With FlexPoint, Utah MSPs gain a fully automated system that streamlines surcharge management, maintains compliance, and protects client relationships.

MSPs can improve financial stability without compromising customer trust by removing manual calculations and providing a transparent, structured approach to surcharging.

Enhance your MSP’s bottom line and compliance with automated credit card surcharging solutions from FlexPoint.

Stay within Utah’s regulations and simplify your MSP payment processes using FlexPoint today.

Schedule a demo to see how FlexPoint can transform your financial operations and maximize profitability.

Additional FAQs: Credit Card Surcharging in Utah for MSPs

{{faq-section}}