According to the Florida Attorney General, “merchants in Florida may add a surcharge to credit card purchases” as of March 2025.

However, Florida’s approach to credit card surcharges has been complicated. While state law technically prohibits surcharging, a court ruling deemed the ban unconstitutional and unenforceable.

Even so, MSPs in Florida must follow specific guidelines when adding surcharges. MSPs must register their surcharge program, clearly disclose the fee to clients through signage and receipts, and ensure the surcharge does not exceed their actual processing costs.

This guide provides Florida MSPs with strategies for implementing surcharges in alignment with federal, state, and card brand rules.

It also covers how payment automation tools streamline compliance and simplify billing processes for transparency and client satisfaction.

Disclaimer: This information is provided for general informational purposes and does not constitute legal advice. Consult a legal professional for guidance tailored to your MSP’s distinctive circumstances.

{{toc}}

What is Credit Card Surcharging for MSPs in Florida?

Credit card processing fees can take a consequential toll on Florida MSPs, particularly those handling recurring payments or high transaction volumes.

Credit card fees typically range from 2.5% to 4% per transaction, covering costs such as interchange fees, network assessments, and payment processor markups.

To mitigate these costs, many Florida businesses use credit card surcharging—a practice where an additional fee is applied to transactions paid via credit card.

Rather than generating a profit, this fee helps MSPs recoup processing costs while giving clients a choice in how they pay.

Those who opt for credit cards cover part of the expense, while clients who choose alternative payment methods—such as ACH transfers—avoid the fee altogether.

Even though surcharging is technically permitted in Florida, it is heavily regulated. Under federal law, credit card surcharges cannot exceed 4% of the transaction amount.

However, Florida MSPs must also comply with card network rules, including Visa, which places a stricter 3% surcharge cap.

Since card network rules take precedence, MSPs in Florida must ensure their surcharge stays within the 3% limit for Visa transactions and 4% for other transactions. These fees can also never exceed the actual cost of processing the payment.

To illustrate the financial benefits of surcharging, consider a Florida-based MSP processing $90,000 per month in credit card payments, with an average processing fee of 3%.

Without surcharging, the MSP pays:

- $2,700 per month in processing fees

- $32,400 annually lost to credit card costs

By applying a 3% surcharge, the MSP passes the entire processing cost to clients, eliminating this expense and preserving over $32,000 per year that can be reinvested in staffing, technology, or expansion efforts.

Alternatively, if the MSP chooses a 1.5% partial surcharge, they would recover:

- $1,350 per month from clients

- $16,200 annually while still absorbing half of the original processing cost

This approach reduces expenses while softening the impact on clients who may be sensitive to additional fees.

Regardless of the surcharge amount, MSPs in Florida must ensure full transparency in their billing practices.

Clients must be informed about surcharges before payment is processed, with clear disclosures on invoices and billing statements, payment portals, and checkout pages.

The following sections will outline Florida-specific regulations and provide best practices to help MSPs implement surcharging correctly while avoiding penalties and payment disputes.

Understanding Credit Card Surcharging Laws in Florida

Florida’s no-surcharge law (Fla. Stat. §501.0117) was ultimately ruled unconstitutional by the Eleventh Circuit Court of Appeals in 2015.

The case, Dana’s Railroad Supply v. Attorney General, Florida, was brought by four small Florida businesses that had received cease-and-desist letters from the state’s Attorney General for adding credit card surcharges.

On appeal, the Eleventh Circuit found that Florida’s law violated the First Amendment, reasoning that it targeted how a price difference was communicated rather than the pricing itself.

In other words, surcharges and cash discounts were deemed the same thing with a different name, so the law effectively punished merchants for using the term surcharge instead of framing it as a discount.

The court concluded that this kind of speech restriction couldn’t survive First Amendment scrutiny and struck down § 501.0117 as unconstitutional.

The Eleventh Circuit’s ruling rendered Florida’s surcharge ban unenforceable, freeing merchants from state penalties for adding a credit card surcharge.

In practice, this means managed service providers (MSPs) in Florida can legally impose surcharges on credit card transactions – provided they comply with federal law and card network regulations (e.g., limits on surcharge amounts and disclosure requirements).

Importantly, surcharges cannot be applied to debit or prepaid card transactions, even if those transactions are processed as credit or if the cards have the Visa or Mastercard logo.

This restriction is mandated by the Durbin Amendment of the Dodd-Frank Act, which governs surcharging practices across the United States, including Florida.

Note: Consult a legal professional for tailored advice on Florida’s surcharging regulations or assistance with developing compliant surcharge policies. Their expertise can help your MSP avoid errors and establish a sound foundation for implementing surcharges.

Implementing Credit Card Surcharging for Florida MSPs

A well-planned surcharging strategy is more than just adding fees—it should be integrated into a broader financial approach to ensure transparency and client satisfaction.

Trust is at the core of any MSP’s business, and unexpected fees quickly damage that trust. Upfront communication about surcharges reduces confusion and positions them as necessary to cover rising operational costs rather than an arbitrary charge.

Clients who understand why a surcharge is applied are less likely to view it as unfair. Proactive discussions and transparent invoicing help manage expectations, preventing frustration and potential disputes.

However, surcharges can also influence client retention.

A recent study by PYMNTS found that additional fees can affect how clients perceive a business, potentially leading them to seek service providers that do not pass on processing costs.

Striking a balance between cost recovery and client relationships is paramount. Billing adjustments should be handled carefully to maintain client trust while ensuring business sustainability.

The following guide outlines practical steps to incorporate surcharges while maintaining compliance and transparency.

Step 1: Establish a Clear Surcharge Policy and Structure

A structured surcharge policy should outline the surcharge calculation method, whether a percentage or flat fee, and how it appears on invoices.

Adding these details to service agreements helps clients understand what to expect. MSPs should tailor their surcharge approach to fit their business and client needs.

Common structures include fixed percentage fees, tiered rates, or flat fees.

Examples of Surcharge Models:

1. Fixed Percentage Surcharge:

A Florida-based MSP applies a 2.9% surcharge to all credit card payments.

Example: A $6,500 invoice would include a $188.50 surcharge, bringing the total to $6,688.50.

2. Tiered Surcharge System:

Surcharge rates vary based on transaction size.

Example: Transactions under $3,500 incur a 2.1% surcharge, while those above $3,500 incur a 3.1% surcharge.

- A $2,800 invoice would include a $58.80 surcharge (2.1%), totaling $2,858.80.

- A $5,600 invoice would include a $173.60 surcharge (3.1%), totaling $5,773.60.

- Flat Fee Surcharge:

A set dollar amount is added to each transaction.

Example: A $60 surcharge applies to all invoices. For a $3,200 invoice, the total would be $3,260.

With any approach, surcharges cannot exceed the processing fee or 4% of the transaction amount, whichever is lower.

For example, applying a $60 surcharge on a $300 payment would violate compliance rules. Instead, the surcharge should be adjusted to $12 or less to stay within regulatory limits.

Flat fees simplify invoicing but require careful monitoring to ensure compliance with Florida regulations.

Florida MSPs can improve profitability while ensuring transparency with a surcharge structure that aligns with their business needs.

Step 2: Notify Credit Card Institutions and Clients

Before you start surcharging, you must inform the card networks in advance. For example, Visa and Mastercard require a written notification at least 30 days prior to instituting a surcharge program.

Visa’s policy explains:

“U.S. merchants must first notify Visa and their acquirer of their intent to surcharge at least 30 days before implementing surcharging. Merchants can submit a notification form to Visa.”

Ensure you submit the necessary notice or online form to your processor and the card brands detailing your intent to surcharge. This step is mandatory under network guidelines, and failing to do so could put your MSP out of compliance.

Once payment networks are informed, MSPs should communicate surcharge policies to clients.

Clients must understand the reasoning behind surcharges and how they apply to transactions. Explaining that these fees offset processing costs—not as a profit source—helps prevent misunderstandings.

Unclear policies can result in pushback.

For example, if a $4,800 invoice includes a $144 surcharge (3%), but the client wasn’t informed in advance, they may dispute the charge. This could lead to a chargeback, causing financial loss and administrative hassles.

To prevent such issues, Florida MSPs should:

- Send an advance email outlining the surcharge policy.

- Clearly display surcharge details on every invoice.

- Include surcharge terms in service contracts.

Thorough communication reduces disputes and ensures clients understand surcharge policies before they are applied.

Step 3: Update Invoicing & Billing Systems

Implement surcharges transparently on all bills and receipts. Configure your invoicing or payment system to add the surcharge as a separate line item whenever a client pays by credit card.

The surcharge line should clearly identify the fee (e.g., “Credit Card Surcharge 3%”) and its amount.

For instance, if an MSP in Florida charges a client $500 for a project and adds a 3% surcharge ($15), the invoice should clearly show the following:

- Services Rendered: $500

- Credit Card Surcharge (3%): $15

- Total: $515

By listing the surcharge explicitly, the client can see exactly why the total increased. This level of clarity ensures the charge isn’t hidden within the price and prevents confusion.

Billing automation tools like FlexPoint simplify surcharge processing by automatically calculating compliant surcharge amounts and adding them as separate line items.

For example, if an MSP processes a $11,000 transaction with a 2.6% merchant discount rate (MDR), FlexPoint will calculate the surcharge as $286 and apply it to the invoice. This reduces manual errors and ensures compliance with both network and legal requirements.

Automation streamlines invoicing and allows MSPs to focus on service delivery rather than fee calculations.

Step 4: Monitor and Review Compliance

Treat compliance as an ongoing task once your surcharge program is in place. Payment regulations and card network policies can change frequently due to new legislation or network rule updates.

For example, Visa only recently lowered its surcharge cap from 4% to 3%, and state-level rules can also evolve. Stay updated on any changes in Florida’s surcharge regulations or card brand requirements.

Regularly audit your surcharge practices, too. Ensure the fee you charge never exceeds your current processing cost, verify that no surcharges are applied to debit transactions, and confirm that disclosures remain clear.

The Role of FlexPoint in Simplifying Credit Card Surcharging for Florida MSPs

FlexPoint offers payment automation solutions tailored for MSPs, helping them manage fees efficiently while ensuring compliance with Florida’s surcharging rules and card network regulations.

By providing flexible billing options, FlexPoint enables MSPs to streamline payment processing, optimize costs, and maintain transparency with clients.

Payment Plans for Florida MSPs

FlexPoint offers two primary payment options, each designed to fit different business needs:

- Interchange+ Plan

- Customer Surcharge Plan

a) Interchange+ Plan

The Interchange+ Plan structures pricing based on interchange rates, ensuring fees remain predictable and align with the type of credit card used.

For example:

- Visa and Discover transactions often have lower interchange rates, reducing processing costs for the MSP.

- American Express and high-reward credit cards carry higher interchange fees, leading to increased costs when clients pay with these methods.

This plan is ideal for MSPs that choose to absorb credit card fees rather than implement surcharging. With transparent pricing and detailed cost breakdowns, MSPs can manage expenses effectively without adding extra charges to client invoices.

b) Customer Surcharge Plan

The Customer Surcharge Plan allows Florida MSPs to pass processing fees to clients in a compliant and structured manner.

Instead of absorbing the cost, MSPs can apply a percentage-based surcharge to credit card transactions, ensuring they recover payment processing expenses.

Example:

A Florida-based MSP invoices a client $8,000 for IT services and applies a 2.75% surcharge to cover credit card processing costs.

The invoice breakdown appears as follows:

- Service Total: $8,000

- Surcharge (2.75%): $220

- Total Due: $8,220

With this model, the MSP eliminates the burden of processing fees, ensuring the full invoice amount is collected without deductions.

For MSPs looking to balance cost recovery and client satisfaction, FlexPoint also offers a shared-cost model, allowing MSPs to split fees with clients.

This hybrid approach ensures surcharging remains gradual and client-friendly, preventing sudden billing changes that could disrupt long-term business relationships.

Whether the goal is to recover processing costs through surcharging or simplify payments with transparent pricing, FlexPoint provides a compliance-focused, client-friendly solution.

How FlexPoint Enhances Surcharging Compliance and Transparency

FlexPoint automates surcharge calculations, keeping fees within the allowable limits while simplifying invoicing for Florida MSPs.

Automated compliance checks help MSPs apply surcharges correctly, preventing disputes and errors.

Below is an example of how FlexPoint helps a Florida-based MSP apply a compliant 2.85% surcharge to a client invoice.

Florida MSP Client Invoice

Company Name: Your MSP

Invoice #: 037892

Invoice Date: April 1, 2025

Due Date: June 1, 2025

Bill To:

[Client Company Name] [Client Address]

[Client Contact Name]

[Client Email]

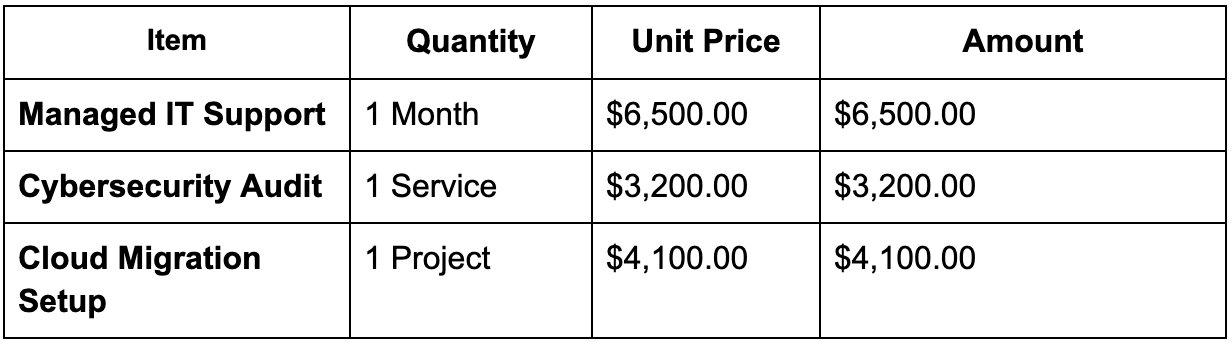

Description of Services

Subtotal: $13,800.00

Surcharge (2.85% of Subtotal): $393.30

Total Due: $14,193.30

Payment Terms

Payment is due within 60 days of the invoice date. The surcharge complies with federal regulations (staying under the 4% federal limit), Florida’s legal environment, and card network guidelines, ensuring smooth, dispute-free transactions.

Notes

Thank you for partnering with [Your MSP]! For questions about your invoice, please contact us at [Your Contact Information].

FlexPoint’s Integration with MSP Tools for Seamless Billing

FlexPoint integrates with leading accounting and PSA (Professional Services Automation) platforms, enabling Florida MSPs to streamline their financial operations while continuing to use the tools they rely on.

Among these integrations are:

- QuickBooks Desktop

- QuickBooks Online

- Xero

- ConnectWise

- SuperOps

- HaloPSA

- Autotask

Seamless integration ensures MSPs can reduce manual data entry, improve billing accuracy, and automate financial processes, making payments and reconciliation more efficient.

This connectivity allows Florida MSPs to automate three essential financial functions known to require significant administrative time:

By automating these tasks, MSPs can redirect time and resources toward growing their business.

Additional features like branded client payment portals and real-time financial reporting enhance visibility and control, allowing MSPs to manage transactions effortlessly.

Offering Flexibility in Surcharging

FlexPoint gives Florida MSPs the ability to customize surcharging practices while maintaining compliance with federal regulations, Florida laws, and card network policies.

This flexibility allows MSPs to implement surcharges strategically, balancing financial well-being and client satisfaction.

MSPs can waive surcharges for high-value, long-term clients while applying them to others, allowing MSPs to prioritize client retention without sacrificing profitability.

Custom rules can also be set for automatic payments. For example, if a client uses Visa, FlexPoint will automatically cap the surcharge at 3%, which aligns with Visa’s guidelines.

Clients benefit from transparent pricing, as surcharges are clearly displayed before payment, helping to minimize disputes and improve billing clarity.

Personalized payment portals also give clients the flexibility to manage their payment preferences.

For instance, a Florida-based IT firm working with a client who typically pays with American Express (which carries a 3.5% surcharge) might find that the client switches to Visa to lower their fee to 3%, reducing costs while keeping payments seamless.

This flexibility ensures a smooth payment process, minimizing friction and ensuring both the MSP and the client benefit from optimized transaction management.

Conclusion: Streamlining Payments with Effective Surcharging Strategies

Credit card surcharging provides Florida MSPs with a practical way to recover the costs of processing credit card transactions, but proper execution is fundamental.

Clients should always know about surcharges before completing a payment. Invoices must list surcharge amounts transparently, ensuring clients understand these fees before they are applied.

Strict adherence to federal, Florida-specific, and card network guidelines ensures surcharge caps are properly followed, preventing unnecessary disputes or compliance risks.

Managing surcharges manually is overwhelming for many MSPs, especially when balancing regulatory requirements, client relationships, and daily operations. FlexPoint offers a solution.

With automated compliance tools, real-time surcharge calculations, and seamless payment processing, FlexPoint enables Florida MSPs to integrate surcharging efficiently without the burden of manual tracking.

Ready to boost your MSP’s profitability with credit card surcharging?

FlexPoint simplifies the entire payment process—helping you comply with Florida’s regulations while improving your bottom line.

Schedule a demo today to see how FlexPoint’s automated solutions can transform your payment processing and drive success for your MSP.

Additional FAQs: Credit Card Surcharging in Florida for MSPs

{{faq-section}}