US consumers disputed over $65 billion in credit card charges in 2023, and the average cost of a dispute grew by 16%. Mastercard also estimates that each dispute costs the issuing bank and the merchant $15 to $70 in operational costs.

Considering the potential financial implications of chargebacks and other payment dispute costs, your business needs a comprehensive strategy to prevent or resolve them.

In a payment dispute, a cardholder claims an invalid transaction on their account. They can cite several reasons for doing so.

The cardholder (an MSP client) might not believe the service they paid for was provided as promised by the MSP. Then, they contact their issuing bank to dispute this charge.

Depending on how you handle this dispute, you could lose the profit from the disputed transaction and not be reimbursed for the associated transaction fees. Beyond these costs, you also risk paying chargeback fees and arbitration fees.

These costs can add up quickly, as you will learn in this article.

This article discusses the costs of payment disputes, explains how to resolve them, and why it’s essential to do so quickly.

10 Common MSP Payment Dispute Challenges

Understanding the challenges related to chargebacks is vital before moving on to resolving MSP payment disputes.

These are 10 of the most common challenges of MSP payment disputes.

1. Delayed Payments

In a 2022 survey by Chaser, 87% of businesses reported that their invoices are paid late.

In the case of a payment dispute, you risk having clients pay late while the dispute is resolved. Depending on the resolution, you might not receive this payment at all.

This uncertainty poses several challenges in terms of cash flow and financial planning.

For example, an MSP that provides monthly IT services to a mid-sized business sees this business has yet to pay for the last three months of service.

During this time, the MSP still has to cover operational costs without the expected revenue. The MSP dips into cash reserves or secures short-term financing (such as loans) to meet its financial obligations.

Without this revenue, the MSP might delay investments in new technology or hiring new employees. Both can impact the quality of service provided to other clients, potentially leading to further financial losses from losing business.

Resolving the payment dispute and returning the funds to the MSP can help restore normal business operations.

However, if the delayed payments become non-payments due to disputes, the MSP could face even more severe financial stress.

Here are just a few examples of the kinds of financial fall-out this MPS might then experience:

- Increased Debt: The MSP might need to take on more debt to maintain operations. This leads to higher interest expenses and weakens overall financial stability.

- Operational Cutbacks: Without this expected revenue, the MSP might have to reduce essential services, delay upgrades, or cut back on labor. Any of these can diminish service quality and client satisfaction.

- Damaged Reputation: Consistent financial instability and an inability to meet client expectations affect the MSP’s reputation, which makes it struggle to attract and retain new clients.

- Business Closure: Prolonged financial stress can force the MSP out of business if it cannot recover the disputed funds or find alternative revenue sources.

2. Billing Errors

One study found that 20-40% of payment disputes are due to merchant errors. For businesses that use manual payment processes, these could be human errors.

For example, if your billing or accounting team puts a decimal in the wrong spot on an invoice, adds or excludes a zero, puts the wrong payment date, or makes any other mistake – any or all of this can lead to payment disputes.

If a client expects to be charged $10,000 for a month of MSP services because that’s what their invoice said, they will likely raise a dispute when charged a different amount.

In this case, your accountant may have accidentally processed an $11,000 payment instead of the $10,000 the client agreed to. Even if this mistake is relatively easy to rectify, it can still damage a client's trust in you.

If the $11,000 figure were used for budgeting and financial planning, your business would have $1,000 less cash flow than expected.

While $1,000 might not make or break your business, ongoing discrepancies can lead to cash flow issues.

Inadequate cash flow has many consequences, ranging from your business being late on payments, being unable to pay employees, or lacking the funds for any other operational expense.

There is a straightforward solution to preventing manual payment errors, which will be discussed later in this article.

3. Service Misunderstandings

If your client's understanding of the scope of services you provide differs from what they receive, this can lead to payment disputes.

If a client sees a charge on their statement for a service they do not believe they received, their instinct might be to raise a payment dispute.

For example, your client sees a charge for “extended support” and immediately calls their bank to dispute it because they did not expect it and believe it was a mistake.

However, you could have clarified the situation if the client had contacted you instead.

You could explain that the "extended support services" refer to the extra hours of consultation you provided during a project last month. You could detail how and when these services were rendered and how they had agreed to this in their contract.

Sometimes, your clients simply do not fully comprehend the services they are (or are not) paying for.

In other cases, your onboarding process may not have been comprehensive enough, leaving your client with questions about the services they do or do not pay for.

4. Contractual Discrepancies

Similar to service misunderstandings, clients might also misunderstand the written contract terms they agree to. This leads to a misalignment in their expectations versus the services they receive.

Several different types of contractual discrepancies can arise.

Here are three examples of contractual discrepancies that can result in payment disputes:

A Client Believes They Were Charged Extra for Services Already Included in Their Plan

An MSP signs a contract to provide IT support to a client. The contract specifies that the MSP’s services include regular system maintenance and troubleshooting.

The client assumes the agreement also includes software updates and hardware replacements. However, these are not mentioned in the contract.

When the client is billed for these additional services, they dispute the payment, believing they should have been included.

A Client Misunderstands the MSP’s Financial Responsibility in the Event of an Outage

An MSP agrees to a 99.9% uptime SLA for a client’s network services. However, the MSP failed to meet this number after several outages.

The client disputed their payment because they believed they had not received the services for which they were charged.

The MSP says these outages were due to circumstances beyond its control (such as third-party service failures). However, the SLA terms did not clearly outline how outages beyond the MSP’s control would be handled.

The client interprets this to mean that, regardless of the circumstances being in or out of an MSP’s control, the MSP should reimburse them.

Conversely, the MSP believes that since the contract does not explicitly state that they are responsible for third-party failures, they should not be held liable for those outages. This discrepancy leads to a dispute over the payment.

Additional Charges for Support Outside of Normal Business Hours

An MSP contract includes a clause for additional charges for emergency support outside of regular business hours.

For example, the client had an unexpected IT emergency on a Sunday in a particular month and required immediate assistance.

The MSP provided the necessary support and billed the client according to the additional charges outlined in the contract.

However, the client is surprised to see this extra charge on their invoice because they assumed 24/7 support was included in their contract.

The client insists they were not informed about the additional fees for emergency support. Believing they were overcharged, the client disputes the payment.

5. Unauthorized Charges

Technically, any transaction a client sees on their statement that they did not approve is considered an unauthorized charge.

As we saw in the examples above, this is sometimes the result of simply misunderstanding their contract.

Other times, the charges may be legitimately unauthorized.

Either way, when clients spot these charges, they could dispute the transactions to have them reversed. An MSP may charge a client an administrative fee for processing payments.

They see a charge on their statement from your MSP for $16.99. This charge is described as “administrative fees,” but the client had not agreed to pay those fees.

When the client notices this charge, they dispute it, arguing they were either unaware of this fee or had not agreed to it.

6. Payment Method Disagreements

Payment method disagreements can result in disputes in a few ways.

If your client has more than one payment method on file, they could raise a dispute if they believe the wrong payment method was charged when the first one failed.

If they had signed a contract that stated this was how failed payments were handled, this dispute might have been resolved relatively quickly.

Offering your clients a broad selection of payment methods is convenient for both the client and the MSP.

The more convenient it is for your clients to pay, the less likely they are to delay payments or fraudulently dispute them if they are charged to a card they used because other options weren’t available.

The MSP-client relationship can be damaged if your client can’t choose their preferred payment method. This can mean they are more likely to raise payment disputes.

A 2023 PYMNTS Intelligence research study, conducted in collaboration with Ingo Money, found that businesses offering multiple instant payment methods earn higher customer satisfaction scores.

The study also found that businesses that offer six or more instant payment methods (for money in or money out) recorded one of the survey's highest Customer Satisfaction Index scores.

7. Chargebacks

If your client calls their card-issuing bank and disputes a charge due to suspected fraud or dissatisfaction with your services, this can lead to a chargeback.

Chargebacks occur when MSP clients initiate a chargeback by contacting their bank or credit card company and claim fraud or dissatisfaction with the services.

Chargebacks are more complicated (and costly) than refunds. They lead to revenue loss revenue and additional fees. They can also damage the reputation of MSPs with payment processors.

Because chargeback fees cost businesses more money than refunds, some MSPs acknowledge and accept the chargeback. Otherwise, they present the charge again and continue fighting it.

The associated fees are called chargeback fees or dispute fees in some cases.

Payment platforms charge different fees for chargebacks based on your chargeback-to-transaction ratio. In 2021, Kount reported that the average chargeback-to-transaction ratio was 1.52%.

Consider PayPal as an example. The standard dispute fee they charge for USD transactions is $15. For high-volume merchants, this fee increases to $30 USD per chargeback.

However, you are considered a high-volume merchant if your chargeback-to-transaction ratio exceeds 1.5% and you have processed over 100 sales transactions in the last three calendar months.

As such, you are charged a higher dispute fee of $30 USD by PayPal.

Chargeback fraud fees are even more costly for MSPs: every dollar you lose to chargeback fraud costs you an estimated $2.40.

If you lose a chargeback fraud dispute worth $3,000, it could ultimately cost you $7,200.

There are different kinds of chargeback fraud. For MSPs, two common examples are digital goods fraud and subscription fraud:

- Digital goods fraud occurs when a client accesses and uses your digital services, is charged for them, and then falsely disputes being charged for them.

- Subscription fraud occurs when a client pays a recurring subscription fee for your service. They dispute the cost of this subscription, falsely stating they did not authorize it or that they had canceled it but are still being charged for it.

Resolving these disputes can be costly for businesses. Considering these high costs, chargeback fees motivate MSPs to prevent payment disputes.

Note: Visa now uses the term “dispute” instead of chargeback, but other card networks regard chargebacks as different from disputes.

Chargebacks911 explains the difference:

“A dispute typically starts after a payment card transaction. The cardholder might see a questionable charge on their monthly statement, or they believe the merchant is taking advantage of them. The customer then calls the bank which issued their card to dispute the payment.

If the issuer is able to explain the payment to the customer’s satisfaction, the case will be closed. Otherwise, the transaction dispute is escalated to a chargeback, which is much worse for the merchant.”

8. Recurring Billing Issues

Recurring billing issues happen when services are automatically renewed without your client's explicit consent or awareness. They might then call the bank to dispute charges for services they thought had ended or did not realize would continue.

Perhaps the contracts your MSP clients sign have an automatic renewal clause. This clause states that either party must notify the other of their intention to end the contract at least 60 days before the renewal date.

Your client signed this contract, but a year later, they decided not to renew it. They assume their contract will run out if they don’t pay for the next year of service. Instead, they are charged for the service (per the contract).

Even though you included this clause in their contract, the client disputes the charge, claiming they never agreed to the renewal.

9. Refund Policies

Disagreements over refund eligibility and processes can also arise from unclear terms at the point of sale, leading to disputes. If your client believes they were eligible for a refund and you disagree, they might dispute this charge.

Refunds and disputes are not the same thing, although your clients might assume they are because they can both result in them getting their money back.

To you, however, a refund and a dispute are two different things and have different fees.

These refund fees should be considered in addition to the chargeback fees we have already discussed to highlight the importance of having comprehensive refund policies in place.

In the case of a traditional refund, you might simply be able to return the funds directly to your client.

In a dispute, the money is returned to the client via the bank before the bank gets the money back from you. This extra step comes with the extra chargeback costs outlined above.

Refunds and Transaction Costs

You might not be reimbursed for the transaction costs you paid when a now-refunded payment was first processed after a dispute.

These transaction costs can add up, and they demonstrate the importance of avoiding disputes.

They include

- Interchange fees

- Assessment fees

- Processor markup fees

Privacy Concerns

If your client believes you mishandled their personal or financial information, this can also result in payment disputes.

Clients are increasingly concerned about the security of their data. They could dispute a payment or take legal action if any information was mishandled or they believed it to be.

For example, if your client learns their personal information was exposed in a data breach at your company, they could decide their financial data is at risk and dispute their recent payment.

10 Effective Strategies for Resolving MSP Payment Disputes

The risks of payment disputes are immense, but various strategies can be implemented to either prevent them from occurring or handle them more effectively when they do.

Here are 10 of the most effective strategies for resolving MSP payment disputes.

1. Clear Communication

If you clearly communicate your billing process and related information to clients, miscommunications that lead to disputes will be less common.

For example, even if your client signed a contract that specifies their contract will be automatically renewed if they do not cancel it within 60 days of the policy ending, send them a reminder about this 90 days before the contract ends.

Whether a client forgot about the clause or did not realize it existed, this reminder is helpful and can also provide you with legal backing if they dispute the charge.

Other billing details to communicate include:

- Payment schedule

- Accepted payment methods and their fees

- Payment due dates and grace periods

- Late payment fees

- Cancellation policies

2. Accurate Invoicing

If your invoices contain errors, such as costs or payment due dates, your client could present this inaccurate invoice to support their dispute.

Have a checks-and-balances system in place for payment processing and invoicing to identify and correct errors. To prevent these situations, consider switching to an automated MSP payments platform.

According to data from the Institute of Finance & Management, 12.5% of manual invoices contain errors.

Further, manual processes are slower than automated ones; they require 80% more work. So, in addition to more errors, the process also takes more time.

Remember to include detailed information on each invoice that offers your clients the clarity they need about what they are paying for.

Your invoice should list the following:

- A detailed outline of the services you provided

- The costs of these services

- Additional charges broken down one by one rather than lumped into one sum

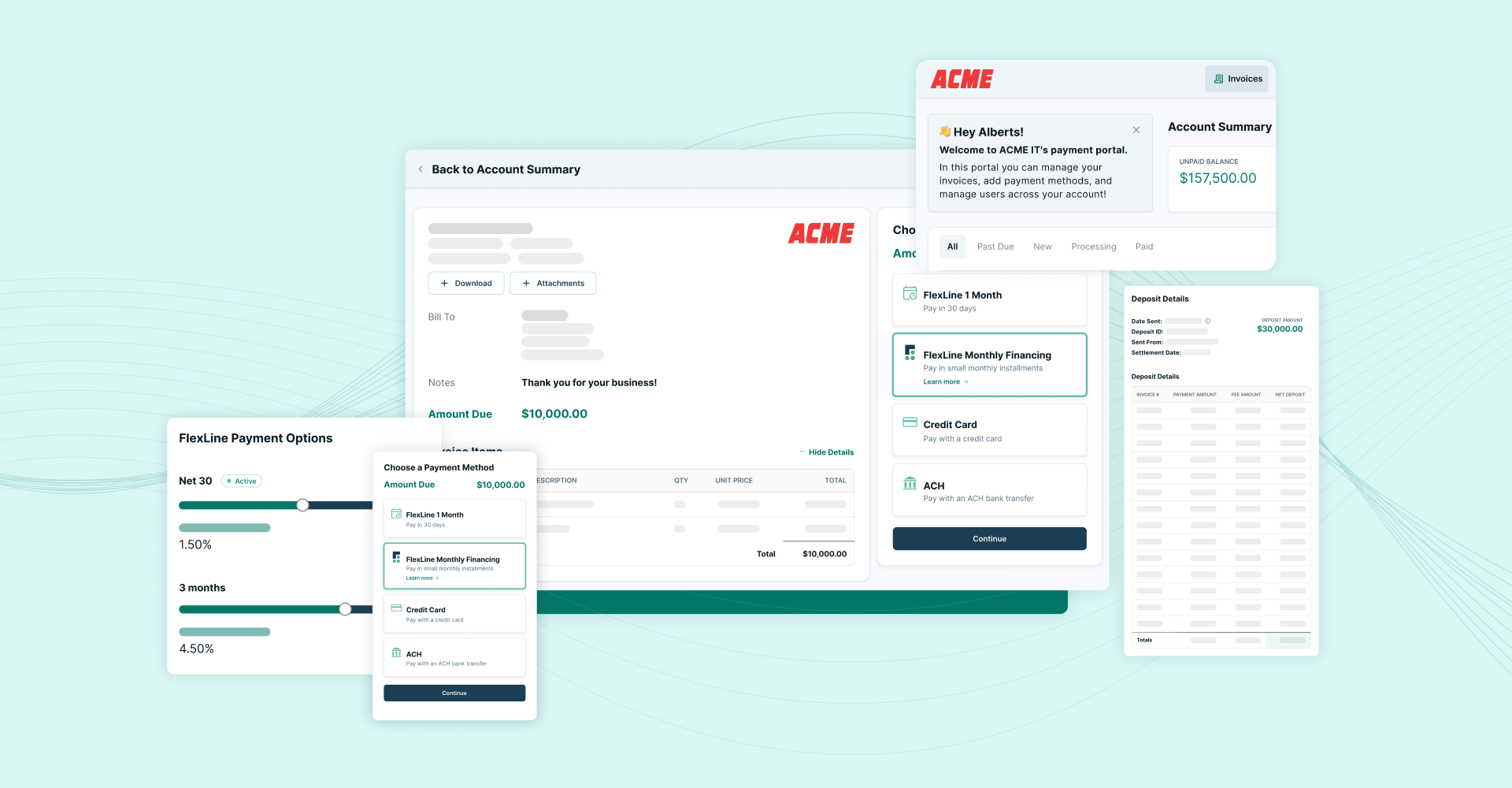

3. Flexible Payment Options

You can better cater to client preferences by offering multiple payment options.

For example, studies published in Statista show that 70% of clients prefer to use a payment method that doesn't share their financial information with their MSP.

The more you can cater to client preferences, the more your client satisfaction rates will be. A study from Microsoft Dynamics 365 supports this claim, explaining that 95% of satisfied clients will be loyal to a business or brand.

A study from Bain & Company also found that a 5% increase in customer retention can produce at least a 25% increase in profit.

Another way to offer payment flexibility is to give your clients the option of installment plans. You might offer this upfront or if a client expresses concern over upcoming payments.

By dividing their payments into smaller amounts spread over time, you can help your client meet their financial obligations and prevent the risks of disputes and chargebacks for payments they make.

4. Robust Contract Management

Contracts must include essential information clients must know about payments for clients to understand. However, these contracts must also outline this information clearly and make it accessible.

For example, consider the 60-day automatic contract renewal clause. If this clause is in fine print or written in unclear language, a client is less likely to read or remember it.

Instead, use the most straightforward language possible for every contract clause and review each with your clients. You might have them initial beside each contract, reaffirming their understanding.

Make your contracts easily accessible to clients so they can easily review them.

For example, if a client believes they should not have been charged for an automatic renewal, they could refer to their contract and see that, in fact, they did agree to this.

5. Proactive Dispute Resolution

A proactive dispute resolution process helps you handle disputes quickly and effectively. It also demonstrates to your clients that you take their concerns seriously.

One way to implement a proactive dispute resolution process is to create a specific email address or team to handle disputes. Your client can directly contact you about potential or existing disputes, allowing you to deal with these issues faster.

For example, a client might contact you about a mistake on their invoice that displays a different amount than what they were charged.

You could proactively refund the payment if they contact you before disputing this payment with their card-issuing bank. Then, you can save yourself the chargeback and dispute fees you might otherwise pay.

6. Client Education

If you provide your clients with the information they need about your billing process and services up front, they will not have to come to you looking for it.

Educating your clients about the details of your services and payment process will also reduce confusion. As we’ve seen, confusion can lead to payment disputes and damage client relationships.

Keep your clients informed by going over their contracts with them in detail. Spend extra time on anything in the contract relating to payments, including payment dates and your dispute resolution process.

Sending your clients notice of upcoming payments can also reduce the likelihood of disputes.

If your client is unsure of why you intend to charge them for a service or what an upcoming payment is for, they can contact you for clarification before their confusion becomes a dispute.

7. Use of Mediation

When you know you have a strong case or a significant financial incentive to win a payment dispute, mediation might be the next best step.

Sometimes, you stand to earn back a significant sum if a dispute is ruled in your favor.

Then, the financial incentive can be worth risking the costs of chargeback arbitration. This means a third party from the card network is brought in to review the case and make a decision.

According to data from Chargebacks Gurus, chargeback arbitration fees average about $500.

8. Implementing Technology Solutions

%20(1).jpg)